Why NRIs Should Be Investing in India Right Now

Geopolitical tension, currency volatility, and a strong domestic growth story are quietly redirecting NRI capital back home. Here is why the smart money is already moving.

Key Takeaways

- NRI investment into Indian real estate hit $14–15 billion in 2024 and is projected to reach $18–20 billion by 2025–26.

- A stronger dollar versus the rupee means NRIs are effectively buying premium Indian assets at a discount.

- RERA, institutional capital, and a 59% jump in PE inflows have made the market far more transparent and credible.

- The window is about timing — capital flows home when global uncertainty rises and domestic growth stays strong.

Every few years, global uncertainty resets investment behaviour — and we are in one of those moments again. Rising geopolitical tension, sharp currency swings, and shifting interest-rate cycles are forcing investors everywhere to ask a single, uncomfortable question: where is my capital safest, and still growing?

For Non-Resident Indians, the answer is becoming clearer with every quarter. After years of parking wealth in Western equities, deposits, and developed-market property, a growing share of NRI capital is quietly turning toward home. And this time, the move is backed by hard numbers — not nostalgia.

The Data Is Already Showing the Shift

This is not retail noise or a seasonal blip. It is serious, structural capital repositioning — and the figures make the trend impossible to ignore.

| Indicator | Figure |

|---|---|

| NRI real estate investment (2024) | $14–15 billion (~20% YoY growth) |

| Projected investment (2025–26) | $18–20 billion |

| NRI share of residential sales in top cities | 18–22% |

| Real estate + construction share of GDP | ~18% |

| Growth in PE real estate investment (2025) | +59% |

When nearly one in five homes sold in India's leading cities is bought by an NRI, the diaspora is no longer a side story in the market — it is a primary driver of it.

Why This Is Happening

- Global uncertainty drives a flight to real assets. When instability rises, equities turn volatile and currency risk increases. Property does not panic — it holds its ground and stabilises a portfolio that may be overexposed to paper assets.

- The currency advantage is real. A stronger dollar (and dirham, and pound) against the rupee has lifted NRI inflows and deposits. For an investor earning abroad, India is effectively on discount — every unit of foreign currency simply buys more.

- India's growth story is hard to ignore. One of the fastest-growing major economies, with real estate and construction contributing close to 18% of GDP and an urbanising population fuelling sustained housing demand. You are not just buying a flat; you are investing in India's growth engine.

- The market itself has matured. RERA has brought transparency, accountability, and recourse that simply did not exist a decade ago. Institutional and private-equity capital is flowing back in, and that scrutiny raises the quality bar for everyone.

Where the Smart Capital Is Going

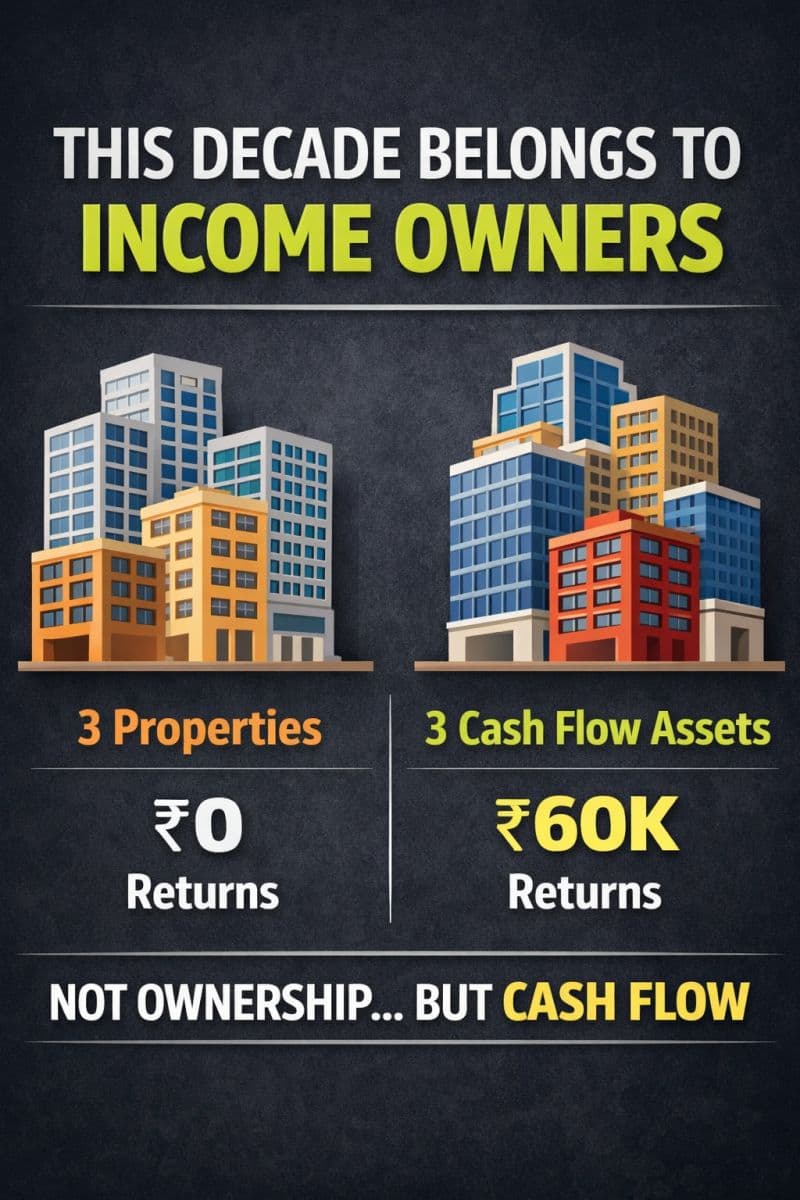

The NRI of 2025 is not chasing trophy bungalows for emotional value. The conversation has shifted decisively toward assets that perform — managed, income-generating real estate in high-demand corridors near IT and commercial hubs. Pre-leased homes, co-living, and serviced studios are attracting outsized interest precisely because they combine three things diaspora investors prize: a tangible asset, predictable monthly cash flow, and professional management that runs without the owner being on the ground.

A Few Practical Points Worth Knowing

- Repatriation is structured, not blocked. Rental income and sale proceeds can be routed through NRE/NRO accounts within RBI guidelines, so capital is not trapped.

- Transparency works in your favour. RERA registration, escrow-protected payments, and clearer title norms reduce the very risks that once made NRIs hesitate.

- Management matters more than the address. For an investor living overseas, a credible operator is the difference between passive income and a long-distance headache.

The Real Opportunity Most People Miss

This is not only about buying property — it is about timing. When global uncertainty rises while domestic growth stays strong, capital flows back home. The investors who benefit most are rarely the ones who wait for perfect clarity; by the time the story is obvious to everyone, the advantage has already been priced in.

If you are an NRI, ask yourself one question: are you chasing returns scattered across the globe, or positioning capital where growth, familiarity, and currency advantage all align at the same time?